In production

Portfolio at-a-glance.

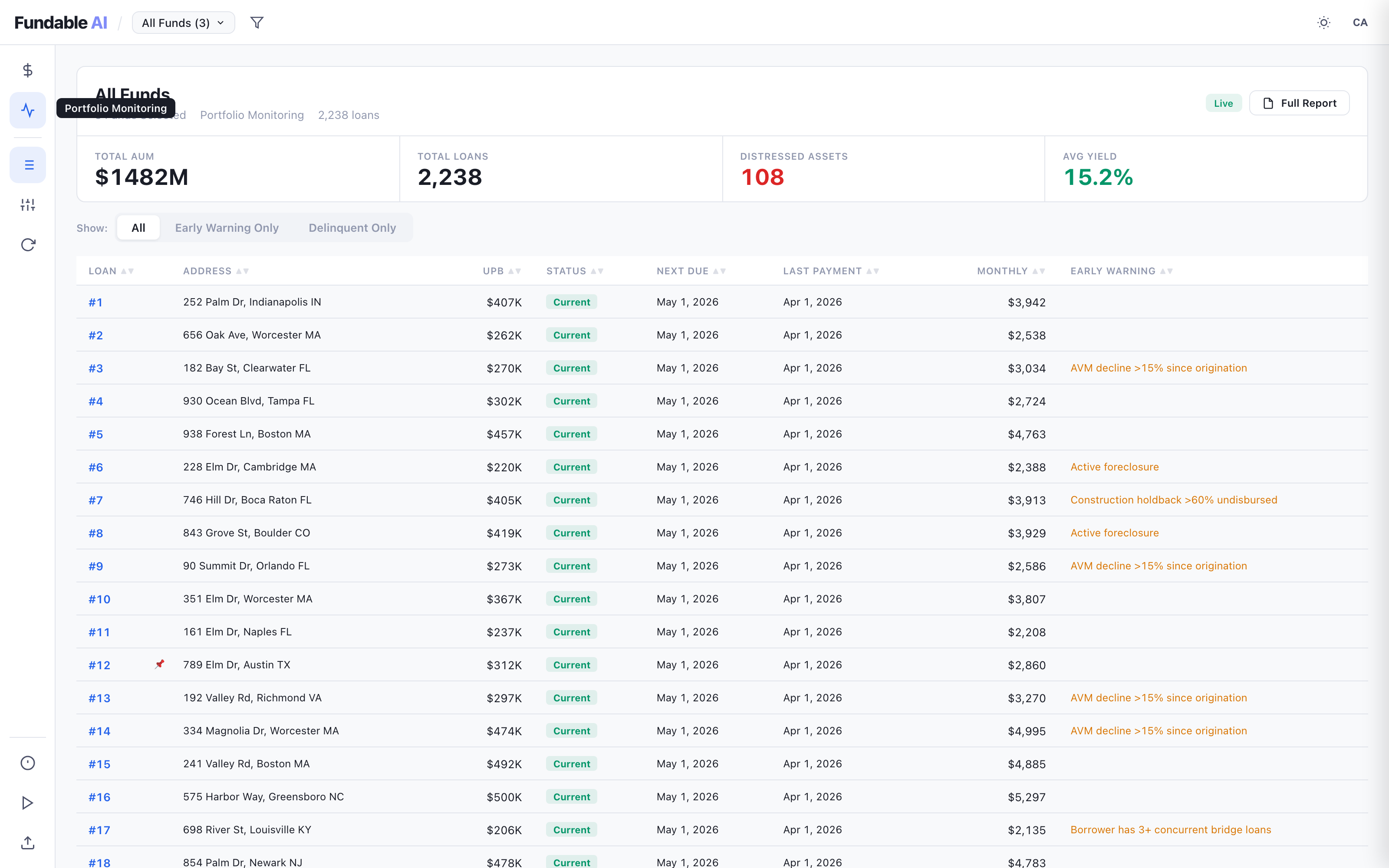

MSR and whole-loan portfolio metrics — UPB, commitment, holdback, WAC, FICO, LTV — with discrepancy flags and per-loan drilldown.

Servicers carry asymmetric duration risk. We hedge it, mark it, and run delivery operations so you can manage portfolio at scale without the audit drama.

Two-faced risk: prepayments in rate-down regimes, mark drawdowns in rate-up regimes. We size hedges that work in both.

Daily marks that hold up under audit, accounting review, and bid-side scrutiny. Methodology documented per position.

Sub-servicer transfers, GSE re-deliveries, and acquisition boarding handled with full chain of custody.

Use them à la carte or as an integrated stack — most servicers start with hedging and expand.

Two-faced duration management. Models MSR risk in both rate-up and rate-down regimes simultaneously, then hedges the asymmetry.

Daily mark-to-market on whole loans, MSRs, and structured credit. Audit-ready methodology and inputs on every mark.

Sub-servicer transfers and re-delivery operations with chain of custody — doc completeness, custodian transfers, wire reconciliation.

MSR and whole-loan portfolio metrics — UPB, commitment, holdback, WAC, FICO, LTV — with discrepancy flags and per-loan drilldown.

30-minute call. Walk us through your MSR portfolio, hedging setup, and what's painful at month-end.

Contact Sales